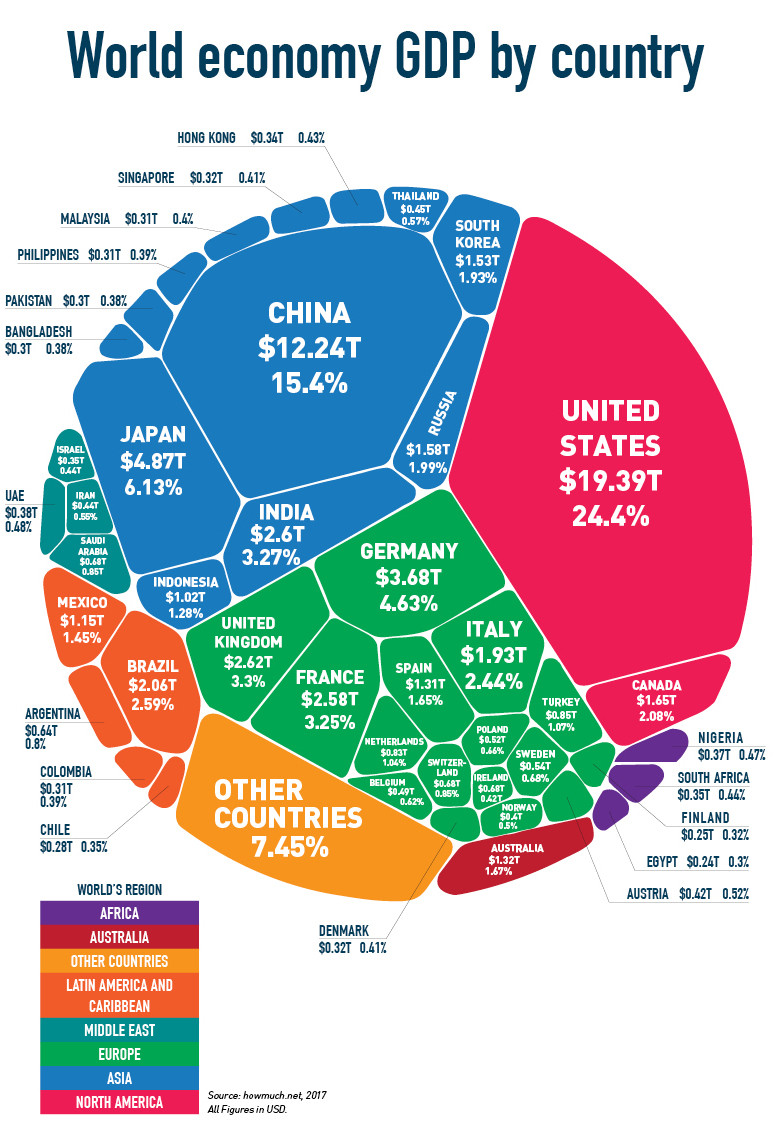

However, in 2016, the International Monetary Fund called the Chinese economy the world’s largest when adjusted for purchasing power parity (which allows you to compare how much your money can buy in relative terms).

Perhaps a more telling statistic is that per capita disposable income is US$39,513 in the US and just US$2,993 in China. This more aptly illustrates just how far China has yet to go to give its citizens a similar quality of life.

The next two largest economies are Japan (US$4.9 trillion) and Germany (US$4.6 trillion). It’s India (US$2.6 trillion), however, which has now passed France and, given Brexit, probably also the UK, which is increasing the fastest. Brazil, despite its very recent economic woes, surpassed Italy in GDP rankings to take the number eight spot overall. Canada rounds out the top ten.

Australia’s GDP was US$1.32 trillion or 1.67% of the global economy, which just about puts it on par with Spain. While punching above Spain and most others in terms of GDP per capita, Australia remains a relatively small economy in global terms.

The infographic below shows the composition of the US$80 trillion global economy in 2017, the most recent year in which comprehensive figures were available. In nominal terms, the US still has the largest Gross Domestic Product (GDP) at US$19.4 trillion, making up 24.4% of the world economy, nearly 60% larger than China at US$12.2 trillion.

However, in 2016, the International Monetary Fund called the Chinese economy the world’s largest when adjusted for purchasing power parity (which allows you to compare how much your money can buy in relative terms).

Perhaps a more telling statistic is that per capita disposable income is US$39,513 in the US and just US$2,993 in China. This more aptly illustrates just how far China has yet to go to give its citizens a similar quality of life.

The next two largest economies are Japan (US$4.9 trillion) and Germany (US$4.6 trillion). It’s India (US$2.6 trillion), however, which has now passed France and, given Brexit, probably also the UK, which is increasing the fastest. Brazil, despite its very recent economic woes, surpassed Italy in GDP rankings to take the number eight spot overall. Canada rounds out the top ten.

Australia’s GDP was US$1.32 trillion or 1.67% of the global economy, which just about puts it on par with Spain. While punching above Spain and most others in terms of GDP per capita, Australia remains a relatively small economy in global terms.

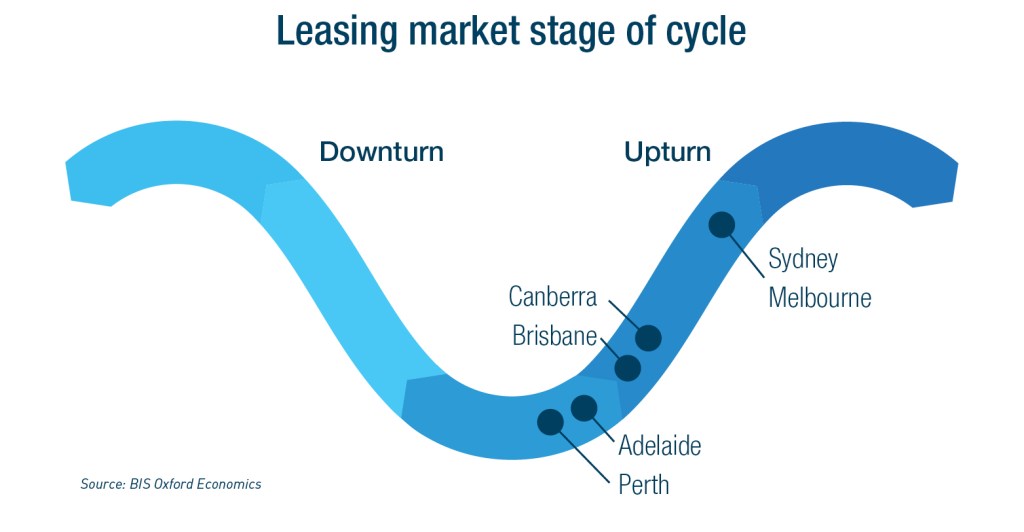

Why diversify?

Australia has often been called the lucky country, given its more than 25-year run without recession. Luck, however, is not a strategy, nor is it sufficient to build a business, execute a strategy or pay distributions. Luck can run out and, diversification, whether or not it’s for personal investing or growing a business, is important.

Diversification doesn’t mean turning your back on what you know or are familiar with (Australia), but it does mean prudently assessing opportunities which can diversify investment portfolios or business income streams both by sector and by geography.

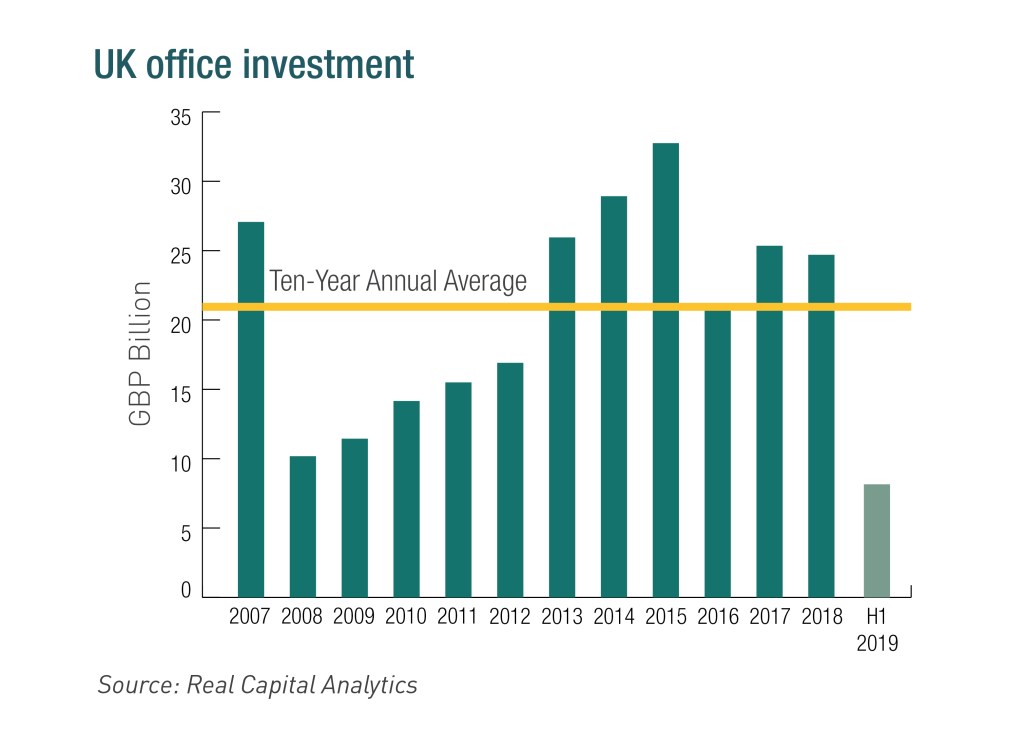

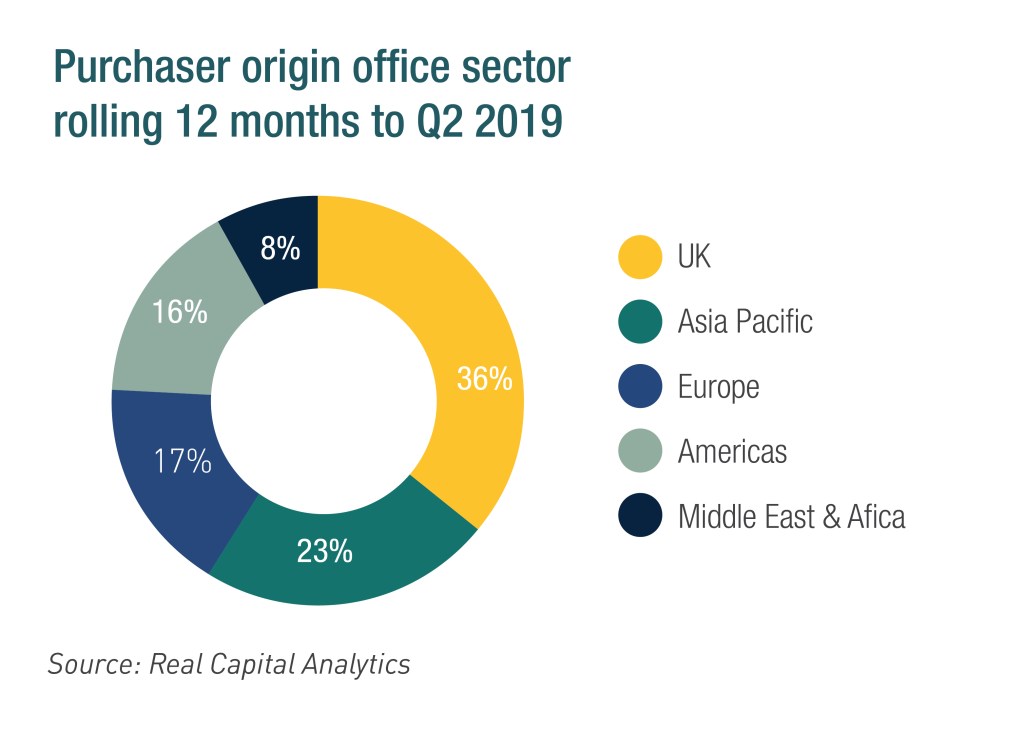

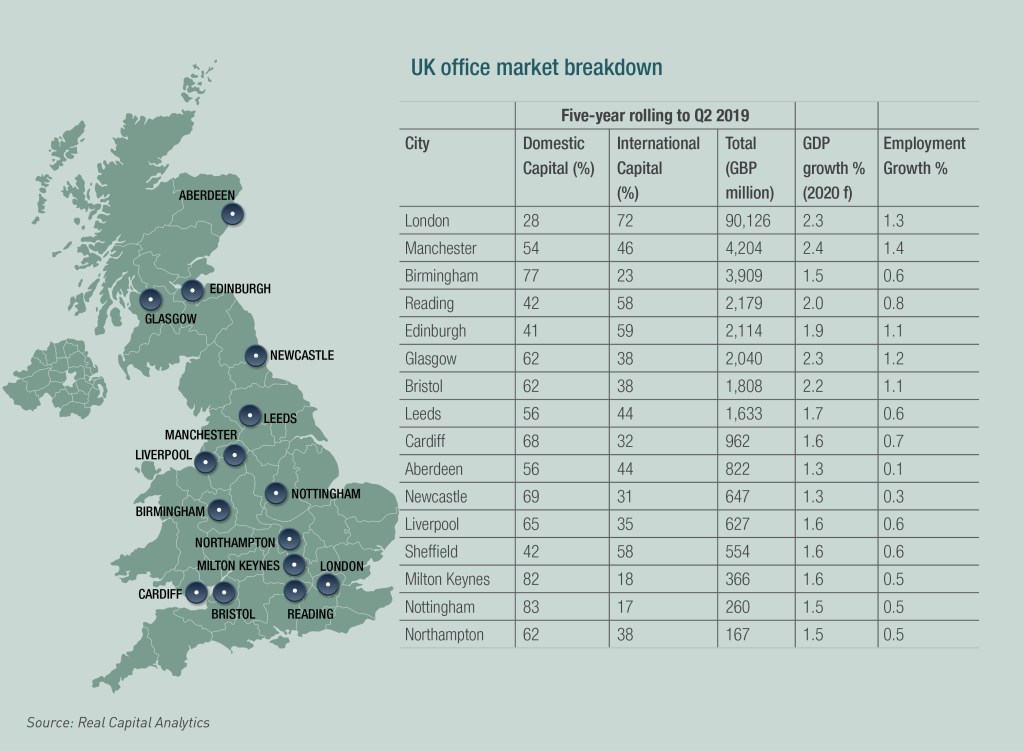

The European real estate market, for example, comprises approximately 350 million sqm of office stock, over 14 times more than the Australian equivalent. The market comprises more than 34 different individual office markets, each with more than 2 million sqm of office space.

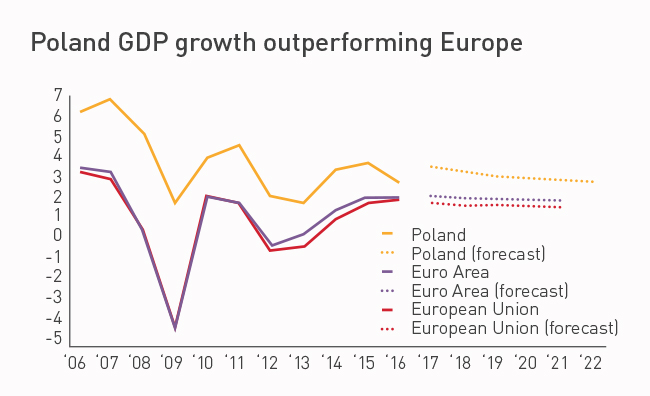

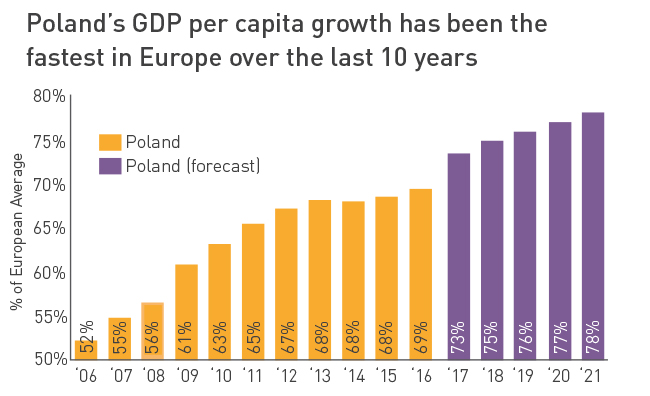

To put it in perspective, that’s 34 different markets the size of Brisbane or Canberra that you can choose to invest in. All of these locations will have different local market dynamics, are at different points in the real estate cycle and are in differently performing countries, some of which, like Poland, currently have better prospects than Australia. Diversification matters.

GDP growth remains weak, at 1.4% for the 12 months to 30 June 2019. The key factor remains subdued household consumption. Although lower interest rates and income tax cuts are generally supportive, the Australian consumer seems to have their hands firmly in their pockets.

GDP growth remains weak, at 1.4% for the 12 months to 30 June 2019. The key factor remains subdued household consumption. Although lower interest rates and income tax cuts are generally supportive, the Australian consumer seems to have their hands firmly in their pockets.

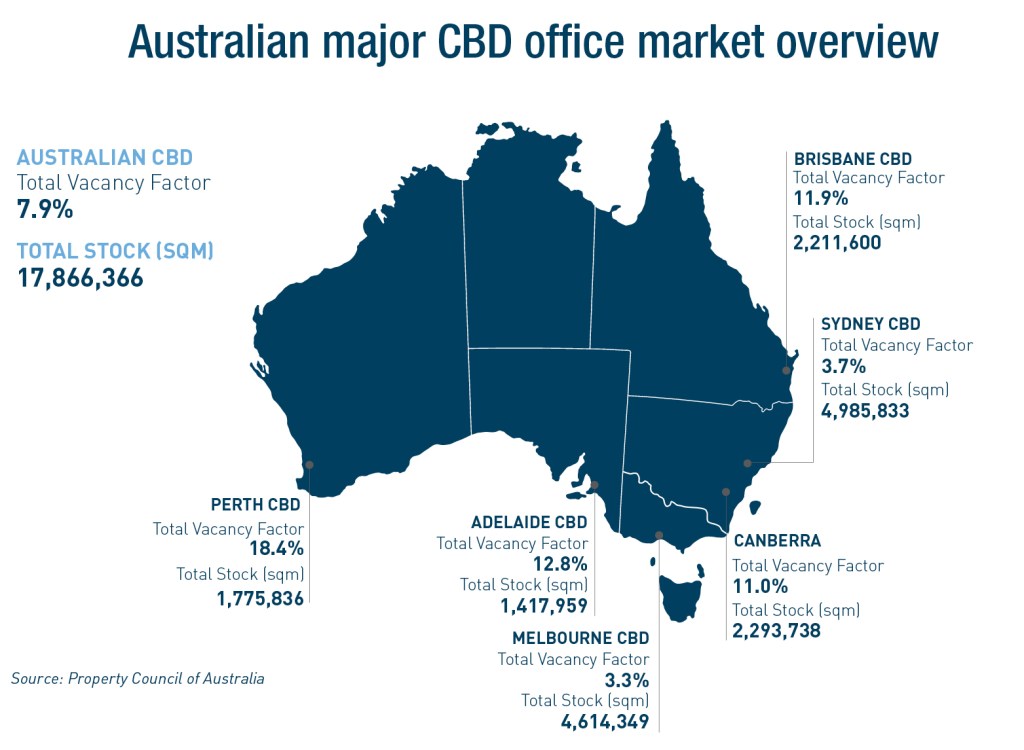

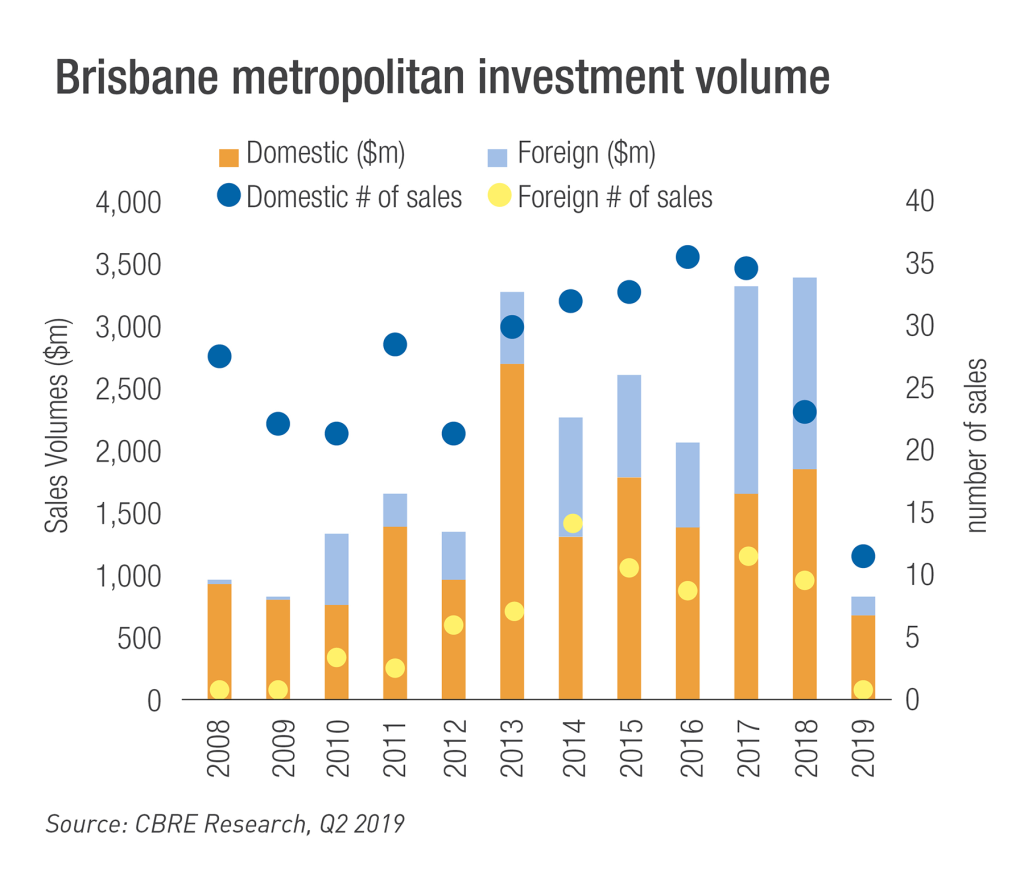

Brisbane CBD comprises over 2.2 million sqm of office stock, making it just under half the size of the Melbourne CBD and slightly smaller again when compared to Sydney. Its vacancy, however, is a lot higher, albeit on a downward trajectory having dropped to 11.9%, from 12.9% just six months previously. Brisbane fringe vacancy contracted from 15.7% to 13.8% over the same period.

Brisbane CBD comprises over 2.2 million sqm of office stock, making it just under half the size of the Melbourne CBD and slightly smaller again when compared to Sydney. Its vacancy, however, is a lot higher, albeit on a downward trajectory having dropped to 11.9%, from 12.9% just six months previously. Brisbane fringe vacancy contracted from 15.7% to 13.8% over the same period.

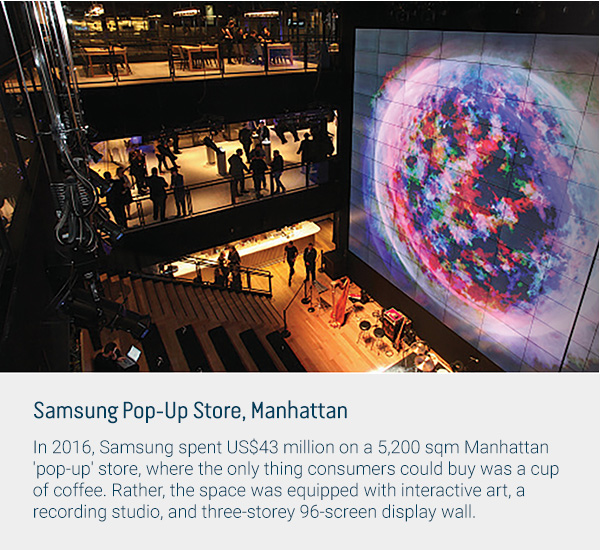

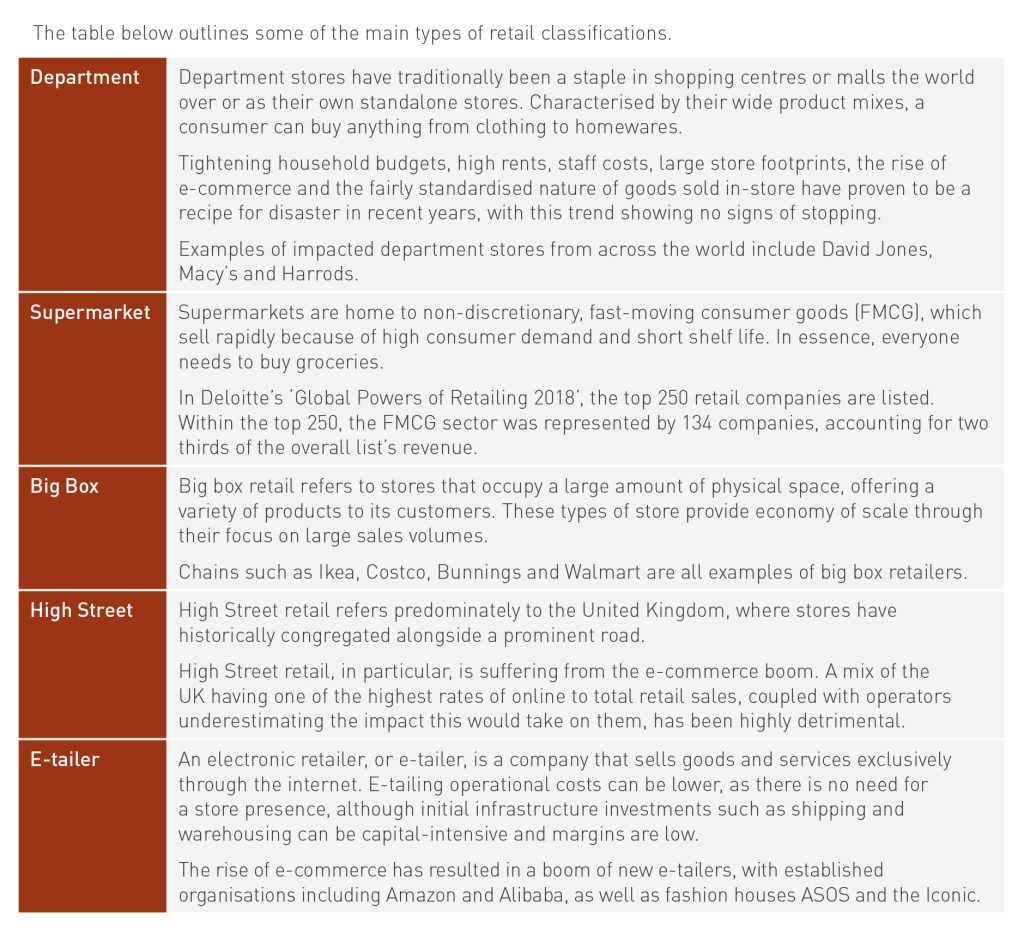

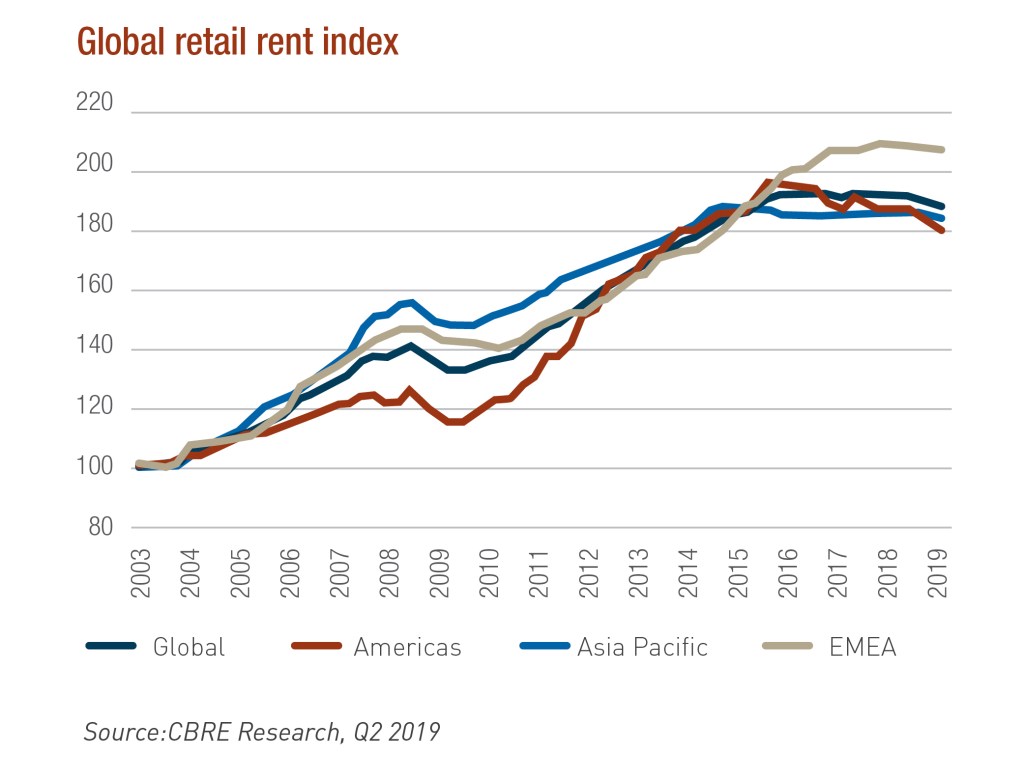

The retail landscape varies dramatically from country to country. The United Kingdom is the home of high street retail, where the United States is the land of not only the free, but also the shopping mall and has more shopping space per person than anywhere else in the world.

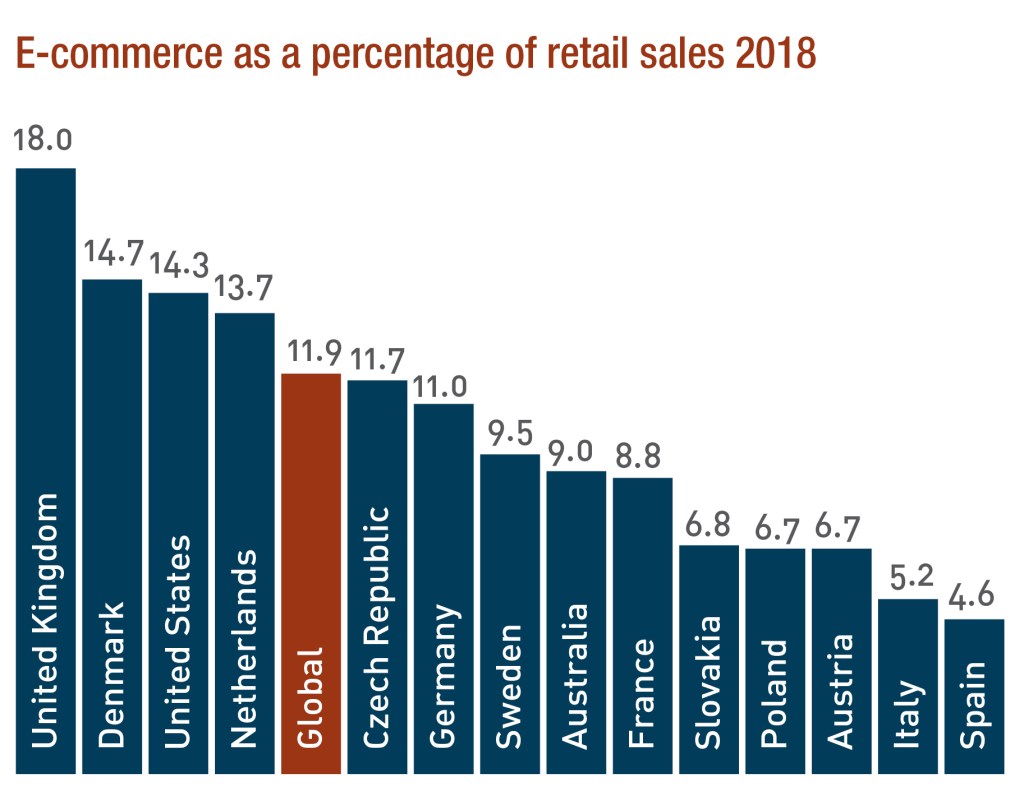

The retail landscape varies dramatically from country to country. The United Kingdom is the home of high street retail, where the United States is the land of not only the free, but also the shopping mall and has more shopping space per person than anywhere else in the world. As online sales reach 11.9% of total retail sales globally, up from 7.4% in 2015 and forecast to reach 17.5% by 2021, there seems to be no sign of a reprieve for traditional operators who have not embraced the internet.

As online sales reach 11.9% of total retail sales globally, up from 7.4% in 2015 and forecast to reach 17.5% by 2021, there seems to be no sign of a reprieve for traditional operators who have not embraced the internet.

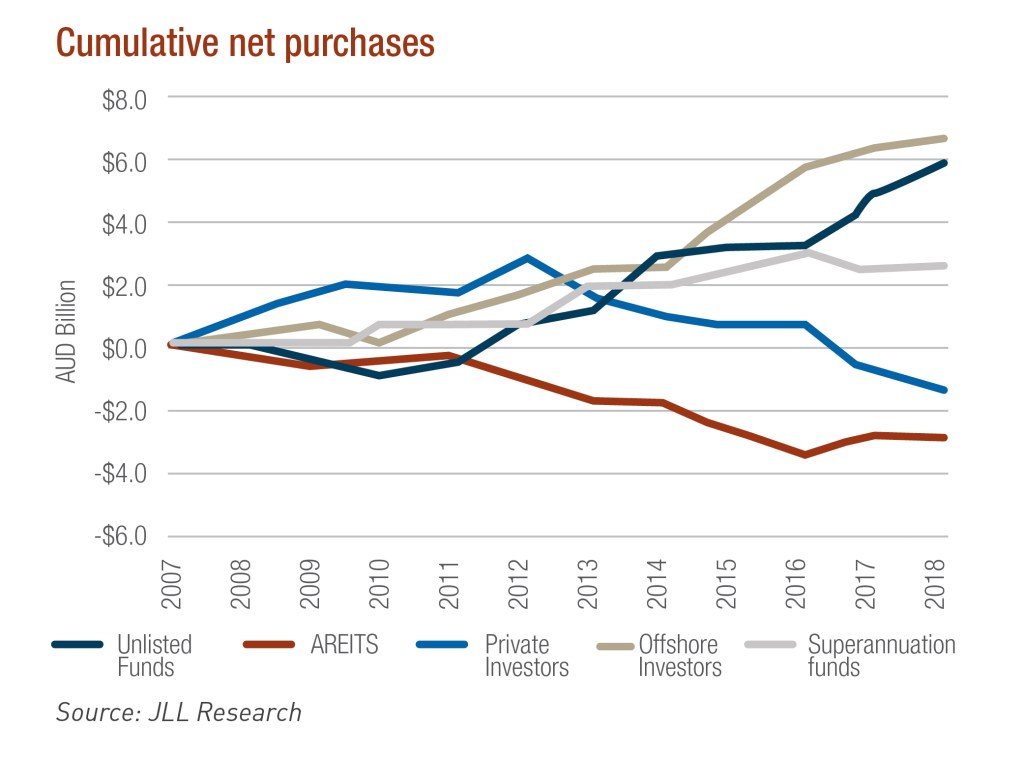

Capital: Influx or in flux?

Capital: Influx or in flux? Omni-channel retailing

Omni-channel retailing