February 26, 2026

Cromwell annouces HY26 results

Cromwell Property Group (ASX:CMW) (Cromwell or the Group) announces its financial results for the half year ended 31 December 2025.

Cromwell Chief Executive Officer, Jonathan Callaghan, said: “This has been a successful half-year for Cromwell, with disciplined execution and solid operational performance across the platform.” Key highlights for the six months to 31 December 2025 include accelerated growth, strengthened financial performance, and continued progress across strategic initiatives.

Key Highlights

- Growth accelerated with the acquisition of an industrial management platform and a 19.9% stake in a $472 million Australian industrial portfolio (the Cromwell Industrial Partnership (‘CIP’)), establishing the foundation for a core pillar of the Group’s growth strategy.

- Group AUM rose 13.2% to $5.0 billion, driven by the industrial platform acquisition and stronger portfolio valuations.

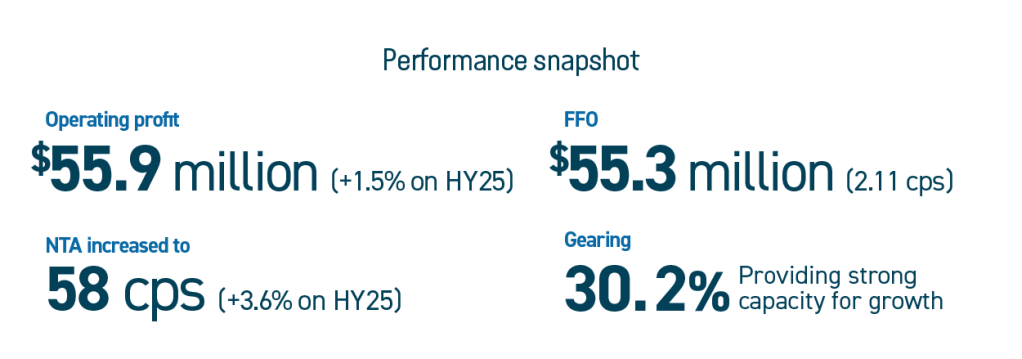

- Operating performance strengthened, with operating profit up 1.5% for the six months ended 31 December 2025.

- The Group’s strong balance sheet provides financial flexibility for growth, with gearing at 30.2%1, significant liquidity of $418 million, and 71%1 of debt hedged, all as at 31 December 2025.

- Investment Portfolio valuations increased by 3.6%1, driven by a successful leasing strategy and high portfolio occupancy of 97.2%1.

- Investment management pipeline continues to build momentum with the Barton1 development progressing on schedule and within budget.

- Distribution guidance of 3.0 cps is reaffirmed for FY26.

We continue to build momentum as we progress our strategy and position the Group to deliver sustainable long-term growth.Jonathan Callaghan, Cromwell Chief Executive Officer

Financial performance

Cromwell reported an increase of 1.5% in operating profit to $55.9 million, supported by the continued strong performance of the Investment Portfolio, which recorded valuation gains of $72.0 million during the period. The Group reported funds from operations (FFO) of $55.3 million, equivalent to 2.11 cents per security, reflecting a payout ratio of 71.0%.

Net Tangible Assets (NTA) increased to $0.58 per security, up from $0.56 per security at 30 June 2025. NTA remains above the current trading price, highlighting the upside potential relative to the Group’s underlying asset base.

Gearing remains low at 30.2%1, providing substantial balance sheet capacity and maintaining significant headroom against debt covenant limits. Cromwell’s $418.0 million of liquidity supports continued flexibility for disciplined capital deployment into growth initiatives.

Investment portfolio performance

Cromwell’s Investment Portfolio delivered a strong performance over the six months to 31 December 2025, with valuations up 3.6% since FY25 to $2.1 billion1, driven by resilient asset fundamentals and improving market conditions. The uplift reflects both sustained leasing activity across key assets and continued stabilisation in valuation metrics as capital markets regain confidence.

Occupancy remains high at 97.2%1, supported by leasing of more than 23,000 square metres during the period. Material uplift was seen at Cromwell’s asset at 400 George Street, Brisbane, where key leases have been extended to 2030 following the exercise of a three‑year lease option by QLD State Government.

Positive market momentum is expected to continue through the remainder of the financial year, supported by firming demand for high‑quality real estate and constrained supply of office space. Together, these factors position the portfolio well for ongoing stable earnings and enhanced returns for investors as the Group continues its growth trajectory.

Strategic growth initiatives

Cromwell advanced its growth strategy during the half through three key initiatives.

Expansion into Australian industrial real estate

Cromwell completed Phase 1 of its transaction with Straits Real Estate Pte Ltd (SRE), acquiring a 19.9% interest in SRE’s industrial portfolio and its management platform, Terre Property Partners (TPP). TPP adds $567 million in AUM, deep industrial expertise and a proven team, strengthening Cromwell’s on-the-ground capability and supporting further growth in investment management.

Phase 2, launching shortly, will bring additional capital partners to the portfolio as it grows through acquisition and development. The existing seven-asset, $472 million logistics portfolio (cap rate 6.1%) provides scale and diversification, with assets in key logistics hubs of Bayswater (VIC) and Salisbury South and Port Adelaide (SA).

New wholesale fund launched

Cromwell launched the Cromwell Creek Street Investment Trust, with a ~$102 million capital raise underway to acquire 100 Creek Street, a 24-level, ~20,000 sqm Brisbane CBD tower. The asset is 94.3% occupied with a diversified tenant base.

The Fund targets an 8.0% p.a. monthly distribution yield, 100% tax-deferred distributions for the first two years, and a 15% target equity IRR over five years. Independent research has rated the Fund “Recommended.”

Barton1 development progressing to plan

Cromwell’s Barton1 development is forecast to complete on schedule and within budget for mid-2027 completion. The 19,800 sqm office building is fully pre-leased to a Commonwealth Government tenant on a 15-year lease, plus a 5-year option, providing long-term income security. Given the challenging development environment, the fixed-price contract, secured pre-lease, and strong tenant covenant position Barton1 as a rare and compelling opportunity.

Investment Management update

Growth in Cromwell’s Investment Management business was driven by the acquisition of TPP and the 19.9% interest in CIP during the period, and the Group now manages $2.8 billion across Australia and New Zealand.

The Cromwell Direct Property Fund (DPF) holds seven2 assets valued at $470.3 million, with the five direct assets valued at $396.5 million, representing a 1.3% valuation increase since at 30 June 2025. Portfolio occupancy remains high and unchanged at 96.4%, with the portfolio’s cap rate tightening to 7.7%.

DPF has commenced the wind up process following the Periodic Liquidity event voted for by investors in late 2025. As part of this process, the sale of 545 Queen Street settled on 19 December 2025, delivering $77 million in net proceeds after selling costs.

Outlook

The Group has made strong initial progress in implementing its strategy to grow third‑party funds under management, broaden our capability set and investor base, and bring to market new products in the office and industrial sectors, with continued work underway in the retail sector, which remains a key focus.

Capital deployment will continue to support growth through both organic initiatives and targeted inorganic opportunities, with an emphasis on strategic, value‑add acquisitions in Australia’s core sectors in partnership with new, aligned capital partners.

Cromwell will maintain strong occupancy across its Investment Portfolio to support income during the current growth phase, underpinned by targeted leasing campaigns, spec‑suite delivery, and capital works designed to enhance occupancy, grow WALE and rental income.

The Group continues to monitor its capital management position by preserving gearing headroom to enable opportunistic transactions, proactively managing refinancing to protect interest costs and liquidity, and maintaining disciplined capital allocation.

The Group reaffirms its expectation of an annual distribution of 3.0 cents per security for the 2026 financial year.

Footnotes:

- Excluding 475 Victoria Ave, Chatswood, which is classified as held for sale and includes Barton1, currently under development.

- DPF assets are comprised of 5 direct assets and 2 assets in underlying unit trusts.