March 22, 2021

Australian 2021 property outlook

Jack Green

While the economy continues to recover from COVID-19, there are a number of challenges facing real estate investors and owners in the year ahead.

Jack Green

While the economy continues to recover from COVID-19, there are a number of challenges facing real estate investors and owners in the year ahead.

The outlook for the global economy has improved substantially. While the road ahead will no doubt be turbulent, there are better prospects for a sustained recovery, albeit economic growth is largely dependent on COVID-19 vaccine rollouts being successful.

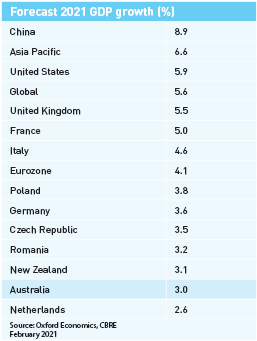

In Australia, GDP is expected to grow 3.0% in 2021 following the first recession in nearly 30 years in the middle of 2020. Positively, the recovery to date has been stronger than anticipated, with GDP now expected to return to its end-2019 level by the middle of the year.

While remote working and hobbies as an alternative to travel, in conjunction with non-discretionary spend, helped prop up the retail sector, service industries such as tourism and aviation will continue to lag.

The unemployment rate has declined to 6.4% according to the Reserve Bank of Australia (RBA), although this is still higher than most of the previous two decades. The rate is forecast to continue to decline to 6.0% by the end of 2021 and 5.5% by the end of 2022.

On 2 March 2021, the RBA announced the cash rate would remain unchanged at 0.1% until actual inflation is sustainably within the 2-3% range. Reaching this inflation target will require a significant improvement in employment and a return to a tight labour market, which the RBA does not anticipate until 2024 at the earliest. As such, the cash rate is likely to remain at an all-time low for some time yet.

While the office sector was heavily affected by COVID-19, other sectors, particularly logistics, have benefitted.

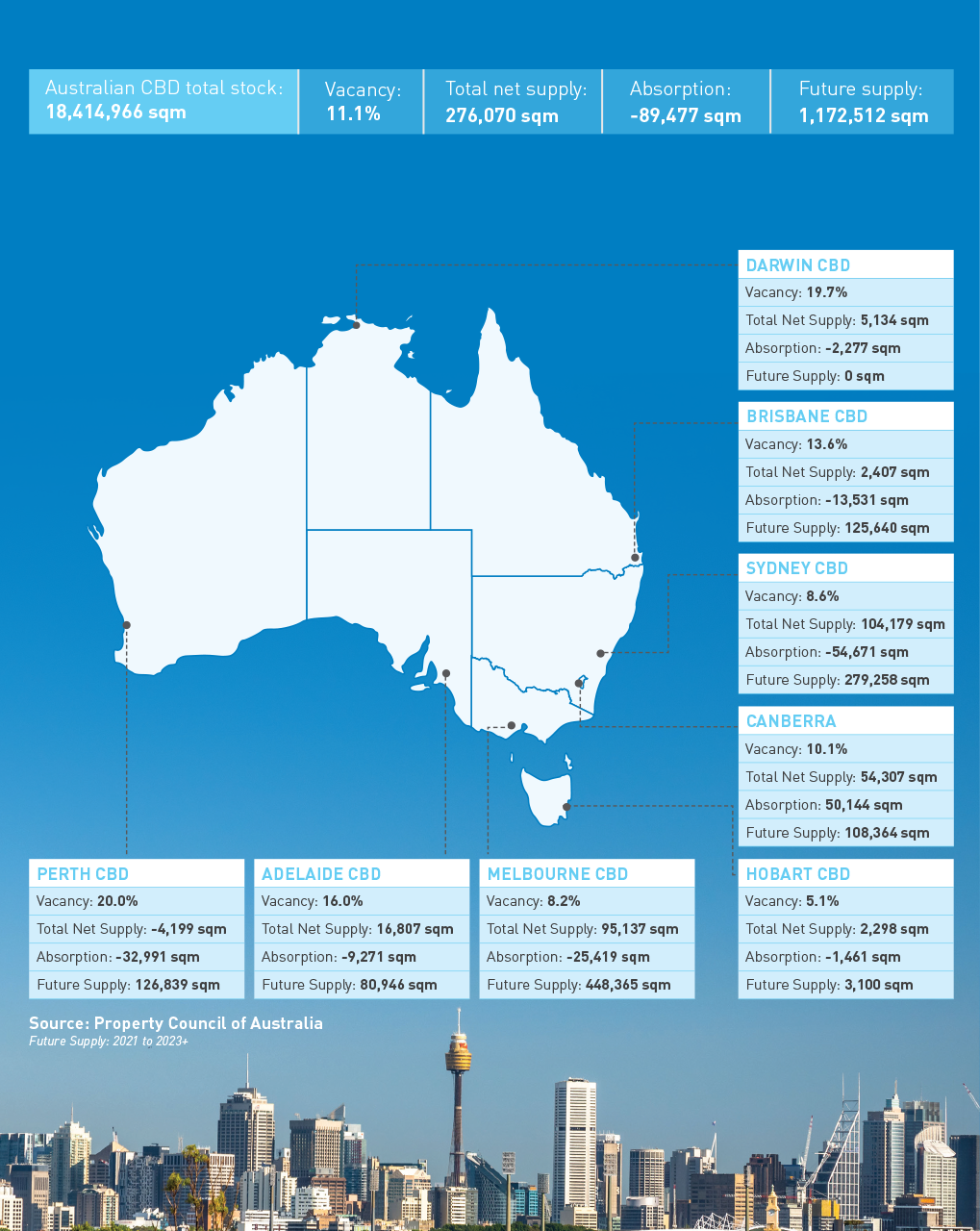

Unsurprisingly, vacancy in Australia’s CBD office markets rose throughout 2020. As at January 2021, the Australian CBD vacancy rate had risen 3.1% year-on-year to 11.1%. Sydney and Melbourne saw their year-on-year vacancy more than double to 8.6% and 8.2% respectively. Brisbane was more subdued, increasing 0.9% to 13.6%.

Despite short-term challenges and much media speculation, the office is here to stay. While landlords supported tenant-customers through the government-mandated Code of Conduct, these measures have now mostly ceased.

A preference for high-quality, technology-enabled and wellness-focused buildings will be of increasing appeal to most potential occupiers. As such, building owners must continue to overhaul workplace design and configurations, strengthen health and safety protocols, adopt smart building technology as well as generally enhance the overall tenant-customer experience. These trends were relevant pre-COVID-19, but have been accelerated over the past year.

A defining theme in 2021 may lie in these value-add opportunities. According to JLL estimates, as much as 40% of existing office stock needs some form of upkeep and investment in order to stay relevant. Consequently, investor appetite for value-add investments is likely to increase.

Although organisations have generally now returned to the office, many have adopted a hybrid model, in which employees split their time between working in the office and working remotely.

A survey conducted by CBRE across Asia Pacific found that more than 70% of managers would prefer to have office-based staff. This infers a disconnect between organisations and their employees, however, the rapid urbanisation and infrastructure improvements across CBD fringe locations have resulted in the emergence of decentralised business hubs which might be able to bridge this gap.

JLL’s ‘Future of the Office’ survey found a hub-and-spoke model might be a suitable compromise between remote working and a lengthy commute to the office. Across Asia Pacific, 31% of companies are contemplating adopting this model, with a further 30% of respondents stating the pandemic has made it less important to maintain large headquarters in CBD locations.

The shift to e-commerce has accelerated changes in shopping behaviour, pushing retailers to reconsider their sales and distribution strategies and landlords towards experiential offerings, particularly for shopping centres or malls.

Given consumers can buy almost anything, anywhere, shopping centres and the brick-and-mortar stores within them must therefore shift focus to incorporate experiential offerings, rather than the simple, traditional procedure of purchasing things.

Retail success now depends on a sound omni-channel strategy, whereby retailers use their store networks for customer acquisition, brand experience, online order fulfilment, returns and data gathering.

An unforeseen but positive outcome experienced throughout COVID-19 has been the boom to certain discretionary sectors. Hardware, home appliances, electronics and household goods have boomed, first as Australians began working from home, and then as lockdowns lifted, home improvement and hobby goods moved to the fore.

The extent of this was evidenced by JB Hi-Fi reporting a HY21 net profit after tax of $317.7 million, an 86.2% increase on HY20, with online sales up 161.7%, representing 13.7% of total sales for the half. Similarly, Super Retail Group, which owns BCF, Rebel and Supercheap Auto, reported net profit after tax up 201% to $172.8 million, with online sales up 87.3%, representing 13.3% of total first half sales.

Separately and unsurprisingly, non-discretionary retail has so far performed as strongly as anticipated throughout the pandemic, with properties substantially weighted towards grocery and other ‘essentials’ always in demand.

The logistics sector has largely benefitted from the challenges facing the retail sector, both prior to and as a result of COVID-19. The pandemic has accelerated many of the longer-term trends that have facilitated record levels of investment into the sector, such as increased internet penetration rates and the aforementioned omni-channel retailing.

Supply chain resilience will come under scrutiny as companies defend against disruption. Efficiency and evolution will drive the future of logistics assets, particularly through automation and multi-storey facilities. Logistics capital growth is shaping up to be considerably stronger than rental growth in 2021, with yields compressing further in what is a popular and increasingly overcrowded sector.

The road to recovery will have its challenges. Investors must work hard to find good investment opportunities, particularly on the back of trends that have been accelerated by COVID-19. These include assets with value-add potential in the office sector and logistics assets that will continue to benefit from a sharp uptick in e-commerce